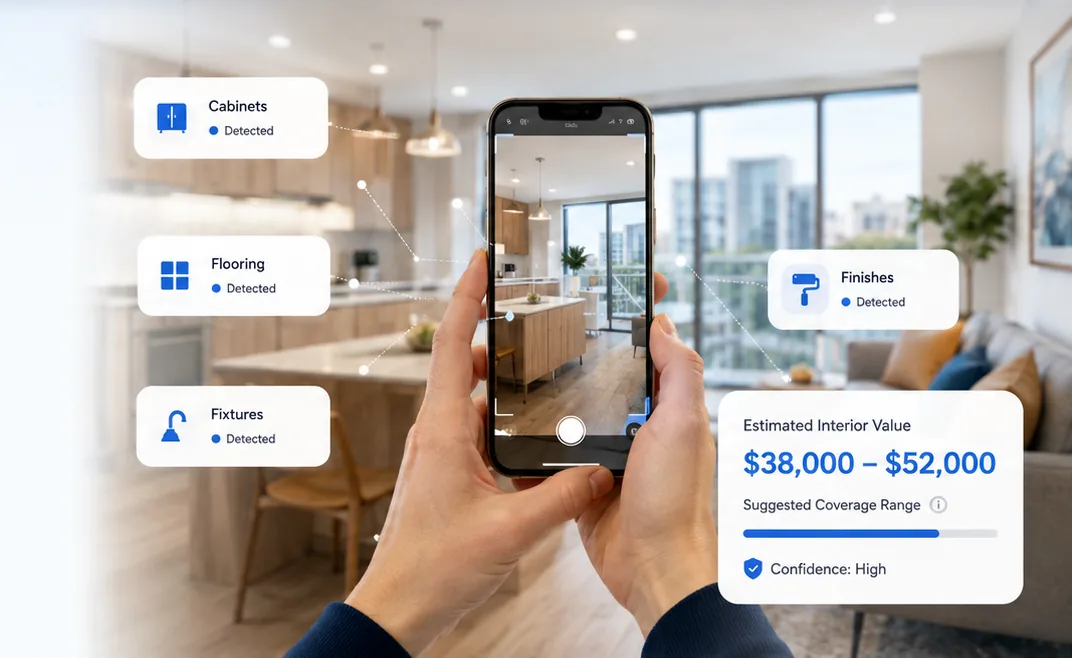

Snap room photos. Get a condo coverage estimate in minutes.

Take room photos. We help estimate cabinets, flooring, fixtures, and finishes.

Often association

Roof, outside walls, halls

The condo association policy often handles the building shell and shared areas.

Often you

Inside finishes and upgrades

Your condo policy often needs to protect what makes the unit finished and livable.

Always confirm

Your association policy

Some associations cover original finishes. Others stop at bare walls.

Step 2 - Optional size check

Add square footage if you know it

The photos do the main work. Square footage is optional and only helps keep the estimate from coming in too low.

What to verify next

Questions every condo owner should ask

Does the association policy stop at bare walls? What does this mean?

Bare walls usually means the association covers the building structure, but you may need to insure inside items like cabinets, flooring, paint, fixtures, appliances, and built-ins.

Could the association charge you after a shared loss? What is this?

A loss assessment is when the condo association bills owners for part of a covered building loss or a large deductible.

Have you upgraded the condo? What counts?

Upgrades can include newer cabinets, stone counters, better flooring, custom closets, built-ins, lighting, bathroom tile, or nicer appliances.

Are contents covered separately? What are contents?

Contents are things you would take with you if you moved: furniture, clothes, electronics, dishes, jewelry, and personal belongings.

What should I ask my HOA for? Show me

Ask for the master insurance policy, bylaws, deductible amount, and whether the policy is bare walls, original specs, single entity, or all-in.

Step 1 - Photo scan

Take photos of each room

Start with one wide room photo, then add close-ups of attached finishes. The AI ignores furniture and focuses on what may belong in condo interior coverage.